PEO Broker FAQs

Why You Need a PEO Broker

Top 5 Reasons People DON’T Get PEO Quotes?

- Their broker told them they are terrible.

- They don’t want to spend the time on getting another quote (p.s. it doesn’t take a lot of your time if you use the right PEO broker).

- They love their broker and think PEOs are like getting quote from another insurance broker (but it is far from that – it is accessing bulk buying that your broker doesn’t have access to and doesn’t want you to know about.

- You got a quote years ago and it wasn’t good – (but the industry has changed dramatically after the federal act came out to regulate this industry and technology has allow you do things you couldn’t before, and the private market health rates still keep going up.)

- A major reason to get these quotes is honestly it is your job and now the courts have just made you actually personally liable if you don’t make sure you get the best deals for your employees under ERISA.

What is the Process to Get a PEO Quote and to Make Sure We Pick the Right One?

The truth is it can be really time consuming and confusing even if you already have a PEO and know what you want. Gathering the proper information is not the time-consuming part – that should take about 20 minutes at the most and it is generally the same information you are used to gathering to shop Medical Insurance. The time-consuming part is listening to all the salespeople all sound the same and all asking you the same questions and all telling you how terrific their PEO is, and in may cases filling out different forms with the same information for them. Then part two – they all ask for more information with mostly the same questions and sometimes different forms and questions. That is really annoying. They get you quotes that are kind of hard to compare because the services all sound the same, but how they are actually delivered is incredibly different and for you to really find out this you then need to do a deep dive into each type of service (and of course the medical plans never match up) and then demos. In the end the truth is you still will not know everything you need to know. And if you get past all that you need to read their confusing contracts that all have incredible language in their favor that you can and must change and add to. It goes on and on, and that ignores negotiation for price and modules and guarantees. WOW.

Or you can use one professional third party to do most of this, tell you the truth and get you better prices while still allowing you to do your job and letting them do all the hard work. These are called PEO Brokers – just like you use your insurance brokers – they don’t charge a fee, they work for you, not the PEOs, have wholesale discount prices and they make sure you don’t pick the wrong PEO, if you should even have a PEO at all. One of the most important things is which PEO broker you pick – see other FAQs (hint: only select a PEO who is only a PEO broker, not an insurance agent, and only one that has staff and clout – most are either a small team or a single PEO salesperson.

What are the ways that they get money you would never know?

If someone can’t explain their services to you in a way that a 5th grader can understand, there’s a good chance they don’t understand it enough themselves and are just repeating what they heard from somewhere else. Which would you rather have – someone trying to fool you with complex charts and big phrases, or the straightforward real experience and practical answers of multiple clients with multiple PEO’s with YEARS in the business?

Our team has always been a brokerage company. We don’t charge fees and only earn our money if we find options that are great for you. We don’t just sign clients to get paid off of fees, we genuinely care about getting the best for you and the people you’re responsible for taking care of. Our PEO Consulting services are designed around simple aligned objectives with you and your company.

We are Objective. We are in this, for one thing, to help businesses take better care of their people. Our team has always been a brokerage company. We don’t charge fees and only earn our money if we find options that are great for you. It’s not billable hours and time – it’s results we deliver, or we don’t get paid.

Why is a PEO Broker Cheaper than the PEO Directly?

Why is it cheaper and better to use a PEO broker vs. calling the PEO directly – doesn’t a broker cost me more?

100% the opposite – 1) PEO direct reps cost the PEOs a lot and they add on a lot to your cost – a lot maybe 20%! We cut out that expensive bias change and give you access to our wholesale prices, plus we’re objective so we know the good, the bad, and the ugly – the truth about each. That direct salesman is not telling you the pros and cons of them vs the competition – the sell you the company they work for or they don’t get paid – plus as we said they add on up to 20% over our prices with the same PEO. Also, there are over 700 – how do you know the right ones to pick in the first place – their ads? A quality broker knows – who is right for your size, location, industry, service level needs, and other requirements – and most importantly frankly who will make your life great or miserable.

How Do I Compare PEOs?

There are 700 of them – how do you even figure out the right ones to call to even narrow down the process?

This will address some of the questions, but it really brings up the other questions that you have to think about. Not exactly a checklist but really this gives you an idea of the differences in the complexities of the purchasing process. But don’t be scared – there’s an easy way to do this all – more on that later.

The comparison spreadsheet we use has 48 rows and they are all important. I know we have said this in other FAQs but it’s worth repeating – they sound like they (PEOs) all do everything – they will all check off they do it on your spreadsheet – just ask any direct PEO salesperson from any PEO- they will tell you how the PEO they are working for (currently) is the best – here is the short truth to this fundamental and important question – PEOs encompass so many aspects that are each complicated – from payroll to benefits to HRIS to WC, etc… even if you have one now and you think you know what to ask for it will take incredible time to do the right due diligence on them and that presumes you went to the right ones. What their salesman says, their internet reviews and their glowingly happy client referrals they cherrypick for you is not what you need to hear or internet reviews say or happy client referrals they cherry-pick for you to talk to say is not what you need – even if you had the time to do this time-consuming project, what you need is a professional that really is objective about the companies, has dealt with their problems, knows what is really going on this year with their software or organization. By the way, a PEO broker doesn’t charge a fee for all this – they get you better rates than if you went direct – you fill out fewer forms – and they will do the comparisons between them all.

Why do you need to compare? Because they are so very different from technology, from service, from guarantees, from style, from admin rates, from hidden fees, from benefit plan, and WC and benefit rates and renewals, from compliance help and defense.

What are these called? They’re called PEO brokers they don’t charge a fee they get lower rates and most importantly they’re good and that is the only thing they do and there are big differences between PEO brokers, but the most important thing is they will make sure you did not pick the wrong PEO you could get fired because of it literally.

PEOs Broker vs Going Directly to a PEO Salesperson

You would think going directly to a provider is the least expensive way to shop – but it isn’t, and here’s why.

- Direct sales forces are very expensive – see below for more on how much they cost you. Buying through large channel partners is almost always guaranteed to be less expensive, and give you a better deal. Amazon, Wayfair, Hotel Tonight, Priceline, etc.

- A direct rep only sells that company, and once you call them and get in the PEOs salesman’s Retail pricing Sales system, you are often stuck at higher prices. Don’t get sucked into the rabbit hole before it’s too late!

- Direct sales reps have quotas – the more they charge you the more they make and the closer they are to their quotas. When they’re talking to you, they don’t care about you or your business, they just want to hurry up and close a deal so they can move on to the next unsuspected business owner.

- Direct sales reps don’t have the buying power of a large distributor – see below how much this can cost you in all the fees.

- Direct sales reps can only sell one company – so with that being said do you really think they’ll keep you up to date on that company’s issues, or just recommend one that is better?

- For example – when times get tough they conveniently “forget” to tell you about how they just lost a lot of clients and/or staff, how the modules really aren’t fully integrated, how they’re about to be sold, the ‘new’ software isn’t working well, a bad block of renewals is coming, e They’ll string you along for a client until the absolute last day, and then leave you hanging.

- Do you think they are going fairly spreadsheet all the competition (all fees, services, medical plans) and break it down in a way that lets you accurately see the best option out of all of the ones you have? No – you’ll have to do all of these comparisons on your own and learn how to do it right. The problem is, doing it right isn’t actually the easiest thing to do unless you know the behind the scenes real facts on this business game-changing decision)

- Do you think they will negotiate with all the other competitions as hard as a large distributor? Do you think they even have the power to? (hint: they don’t).

- You use brokers now – for medical, and workers comp – for a good reason. Would you hire someone who’s just painted a small shed in his backyard to paint your house, or would you rather hire a fully serviced professional painting crew? That’s the difference.

- Don’t call direct and get stuck paying retail. As soon as they answer the phone their one objective is to get you added to a spreadsheet as another client, paying way more than they should for a lot less of the services than they should be getting.

- Don’t call direct – People get stuck on average spending 63 hours talking to each direct rep, looking at their demos, and comparing everything. 63 Whole hours? You would definitely be better off spending all that time optimizing and expanding your business, wouldn’t you? That’s almost 3 days’ worth of time just trying to find the right PEOs and Services when you could meet with a broker and get it done in a fraction of the time!

Scooping!

Scooping is something you would never even think to ask! But your Broker sure will!

You most likely charge employees a portion of their benefit costs and hopefully are using a Section 125 Plan (One you have filed and one you submit 5500’s for (that is another story). Under the 125 plan, those contributions are deductible by the employee for Federal and State Income tax. Under Section 125 you as the company would also save money because your F.I.C.A. matching contribution is based on a lower salary.

Scooping is when the PEO charges you a percentage on your employee’s salary, pays the Government the tax on the salary, and keeps the rest! Really? Yes. Who would even think to ask that question – and by the way that percentage of the total employee contributions for all your benefit plans really adds up!

Here’s a simple example:

Your employee makes $50,000 and contributes $10,000 for health insurance (hopefully in real life the employee’s contribution – even for family coverage, is much less, but for this example let’s stick with easy numbers – the point will be the same).

So, your employee will pay Federal and State Tax on $40,000 and Social Tax on $40,000, not $50,000. From the company’s point of view, you saved 7.65% on the $40,000 instead of the $50,000 also. Or did you???

Scooping is when the PEO charges you the 7.65% on the $50,000 – pays the Government the tax on the $40,000 and keeps the rest! Really? Yes. Who would even think to ask that question – and by the way that 7.65% of the total employee contributions for all your benefit plans really adds up!

That is only one example of why you need a professional PEO broker to guide and educate you on what you need to know about each of these PEOs – whether it is their fees, modules, service model, history of renewals, etc. We compare all of it and present it all in one easy place for you to review.

That is why you need a professional PEO broker to guide and educate you on what you need to know about each of these PEOs – whether it is their fees, modules, service model, history of renewals, etc.

Powered by HTML5 Responsive FAQ

PEO Services

What is CPEO? And Why is it Really Important?

SBE479 – is the federal act that regulates PEOs. It created a certification process – thus the C in CPEO. Of the 700 something PEOs only about 30 have actually received this certification. It is a big deal for an employer. In order to qualify they have to pass a great deal of government tests including financial, I.T. security, compliance, audits etc…

It general what it means is your company can receive better tax treatment, not have to pay mid-year F.U.T.A and SUI restarts, qualify for tax credits that a non CPEO will prevent you from receiving , better data security, better software, better compliance protection from the government, make it less likely they (and therefore you) will have any financial problems relating to a PEO and other important protections.

There are several other certificates that PEO will tell you they have (and several of them have great credibility also (like Employer Services Assurance Corporation – ESAC), and some of the larger PEOs that have this certification also have divisions that don’t so you have to know to make sure you are in the CPEO option.

Many of the smaller PEOs can’t afford to go through this process and many of the specialty firms can’t either. Ask your PEO broker, consultant or expert about this.

There’s been a lot of discussion in the HR outsourcing world about certified professional employer organizations, or CPEOs. What are they and why does it matter, you may be asking?

Here’s the express version:

- Being certified means a PEO has applied to the IRS to be certified and after providing extensive information about its financials and other background information, received the CPEO designation from the IRS.

- A CPEO takes on added responsibility related to payroll administration and federal employment tax reporting and payments.

- A CPEO is responsible for paying the federal employment taxes on the wages it pays to worksite employees.

Essentially, it might provide you further peace of mind when working with a certified professional employer organization. Read on to understand the details and how it may affect your business.

CPEOs The bottom line

CPEO’s can won’t steal your money – bonded and audited. If a non CPEO doesn’t pay your taxes with the money you gave them to pay your taxes you will have to pay it twice.

Better security tax credits available. Not necessarily that is service or better benefit rates.

A little background

The Small Business Efficiency Act (SBEA) of 2014 put things in motion when it set out to clarify the relationship between a certified professional employer organization and its customers for the purpose of federal payroll taxes. It is federal recognition that the PEO industry has needed since its early days more than 30 years ago.

A CPEO establishes a co-employment relationship with its customers. In it, the CPEO assumes many of the employee-related employer responsibilities, while the customer continues to manage and run the business.

Here’s a quick overview of the co-employment relationship:

Your company’s role

- Your company remains an employer.

- It maintains control over managing your employees’ daily to-dos and core job functions as well as maintaining your organizational structure.

- Your company’s leadership team remains focused on fulfilling the primary role they were hired for.

The CPEO’s role

- As the co-employer, the CPEO takes on specific employer obligations, as set forth in your service agreement.

- This allows the CPEO to provide benefits and handle functions such as payroll, tax remittance and related government filings.

- Because it acts as an employer for those purposes, the CPEO can assume a greater amount of responsibility than, for example, a payroll company.

Not everyone qualifies

It’s not a simple process to get certified by the IRS, and not every PEO will qualify. Here are some of the requirements of companies seeing certification:

- An audit of their financial statements

- CPA-affirmed documentation that they pay employment taxes in a timely manner

- Documentation that they have positive working capital

- Background reports of their individuals responsible for employment tax payments

The IRS wants to take a good look at the PEOs it certifies because they’re solely responsible for paying employment taxes on wages they pay to worksite employees. Previously, the IRS could have looked to the client company if the PEO did not pay the federal employment taxes. Basically, the IRS wants to be sure the taxes get paid.

Why it matters

The intent of the law was to give more structure to who is responsible for what and how eligibility for certain tax credits is defined. The highlights of the law and how it relates to CPEOs and their customers include:

- Payroll tax liability

- Double payment of taxes

- Retaining specified tax credits

Payroll tax liability

The IRS has traditionally taken the view that in a PEO arrangement, both the PEO and the customer are jointly and severally liable for paying federal employment taxes. Let’s say a small business hired a PEO, paid the invoice, which would have included the employment taxes, and the PEO didn’t pay the employment taxes. Before the SBEA, the IRS could have gone after the client company for the taxes – money that the company thought it had already paid to the PEO.

The SBEA makes it very clear that a CPEO, certified by the IRS, is solely liable for the payment of federal employment taxes on wages it pays to worksite employees. So, once the customer pays the invoice, which includes the federal payroll taxes, to the CPEO, the IRS can’t come back to the customer to collect employment taxes if the customer is subject to a CPEO service contract or agreement. The CPEO is liable, not the customer.

Maintaining tax credits

Because many tax credits hinge on being the employer, oftentimes businesses entering into a PEO co-employer relationship would be concerned about potentially losing eligibility for those tax credits.

The SBEA clarifies a CPEO customer’s ability to maintain certain tax credits when they’re in a CPEO relationship.

There’s a list of tax credits in the SBEA that’s very clear that the customers get to retain within the CPEO relationship. Among them are:

- IRC sec. 41 credit for increasing research activity

- IRC sec. 45R credit for health insurance expenses

- IRC sec. 51 work opportunity credit

- IRC sec. 1396 empowerment zone employment credit

Wage-base restart

As an employer, federal employment taxes must be paid on a certain amount of each employee’s wage – referred to as the wage base.

When a company joins or leaves a PEO mid-year, there has been the issue of paying taxes on the wage base from both the company and the PEO. This is known as an employment tax or wage base restart and occurs when a new federal employer identification number (FEIN) is used. When a PEO begins paying wages (or a company leaves a PEO), it triggers a change in the FEIN of the entity paying wages.

For example, in June, a PEO takes on a new client that has been paying employment taxes since January. In June, the PEO would be considered a new employer under the Internal Revenue Code. So, paying federal employment taxes on the wage base starts over, resulting in double taxes being paid.

Under the SBEA, it’s clear that if you’re a CPEO customer subject to a CPEO contract, the wage base no longer starts over. The CPEO gets to succeed to the wage base of the employees at a customer coming into the relationship, so there’s no longer a double payment of taxes. While there are a lot of other meanings to the term “successor employer,” a CPEO would only be the successor employer with regard to the wage base for payment of employment taxes.

Additionally, if a company doing business with a CPEO pursuant to a CPEO contract or agreement leaves the relationship, it would benefit from the successor employer status and not have to restart the wage base for employees for purposes of federal employment taxes.

Peace of mind

The SBE legislation was a long time coming. It gives structure, guidance and recognition to the PEO industry.

How to Choose a Reliable PEO?

In Goldilocks and the Three Bears, a little girl searches for porridge that’s not too hot, not too cold, but just right. Your search for the right professional employer organization (PEO) requires a similar journey of taste-testing to find the perfect match for your company.

As a co-employer, the PEO you choose will ultimately take responsibility for processing payroll, providing workers’ compensation insurance coverage, providing employee benefits, and a host of other sensitive tasks.

A mismatch between your company’s culture and that of your PEO, or partnering with a financially unstable PEO, can spell trouble both for your company and your employees. The internet abounds with stories of PEOs increasing rates without warning or going out of business without paying employees or payroll taxes.

To ensure the best fit possible between your company and this close partner, you’ll need to conduct a thorough analysis of your potential PEO.

Here are five steps you can’t afford to avoid.

- Check licensing and accreditation

- Ask for references

- Explore the PEO’s online presence

- Assess financial strength and security

- Research the company history

Doing this on your own is fine, BUT REALLY the way to find the best answers to these is to contact a Qualified, Objective, Large PEO Broker – then supplement your research by talking to a representative of the PEO to verify what you’ve read and found out details that may not be found online. Here are some questions to consider:

- When was the company founded? How long has the current leadership team been in place?

- How many years has the company offered PEO services? Are its PEO services its core offering or a sideline to another business?

- Where is the company headquartered? How many other offices does the company have and where are these located?

- How many corporate employees does it have?

- How many clients and worksite employees (i.e., employees of client companies) does it have?

- What is the mission?

- What are the company’s values?

- What credentials does its staff members have?

- Does the PEO have HR professionals in your company’s key locations? If not, what is their expected response time, should you need them onsite?

- How does the PEO usually communicate with its clients? Does it proactively contact clients or wait for clients to call?

- Can you meet the people who will service your account?

- How many clients does an account representative typically handle?

- Can you see your service agreement?

And there are literally 50 other questions you NEED TO ASK THE WILL BITE YOU IF YOU DIDN’T, UNFORTUNATELY. PEOPLE LOSE THERE JOBS WHEN THEY PICK THE WRONG PEO.

Answers to these questions will give you a better understanding of the personality of the PEO and whether your cultures will be aligned in a co-employment relationship. They can also help you determine the stability and sustainability of the PEO.

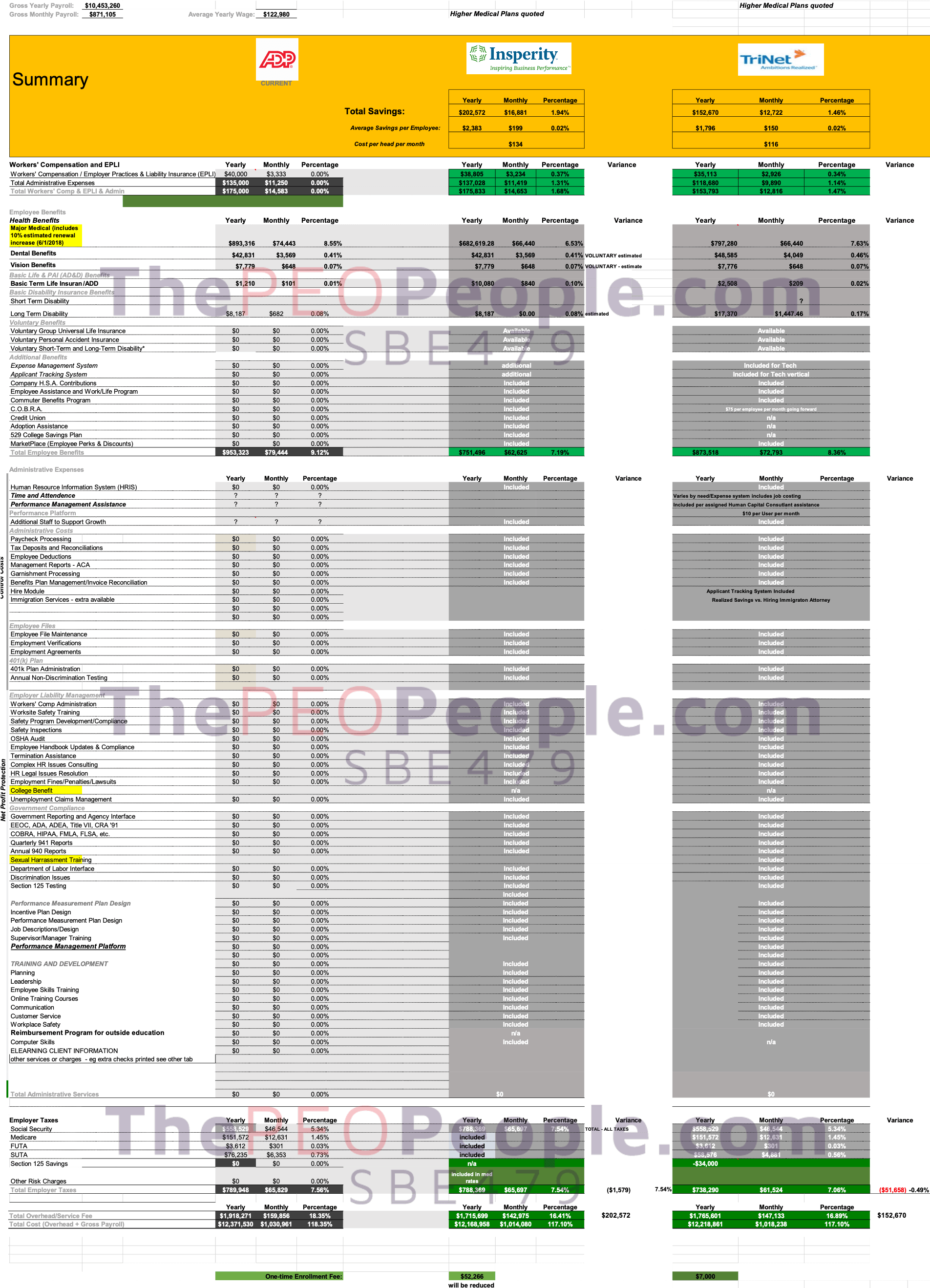

Click here to see a sample of a comparison for a company with 113 employees.

What is a Professional Employee Organization Anyway?

The short answer-

A PEO is the iPhone of human capital – payroll, hr compliance, HRIS systems, time and attendance, performance management, PTO, health insurance and workers comp and unemployment, benefits admin (one bill), easy onboarding – everything annoying, time-consuming and that you can waste money or be sued for – all in one easy integrated bundle that can often save you a ton on health insurance because they are giant buying groups, and a ton of time because it is all integrated, and with HR and legal back up – those are the good ones. The bad ones can make you more miserable. (so how do you make sure you don’t pick the wrong one? – see below in these FAQs)

Watch a quick video here

What is Co-Employment Actually?

This is a term that sounds scary – are PEO’s your business partner, can they fire your people or tell you how to run your business? The answer is absolutely not.

Well, the opposite is kind of true. Co-employment is actually another layer of protection for you under the SBE479 federal act!

In a PEO the federal government defines only certain responsibilities (it is not joint employment) – basically pay your taxes, allow you to be in their group medical and Workers Comp buying consortium, and for some purposes look like they act as an employer of record. This makes them liable for all these issues and therefore they have skin in the game – they will help make sure you are compliant because if something goes wrong and you get sued, so do they. That is why they also provide you with EPLI coverage.

Yes, it sounds unusual, and this is the term that your insurance broker will dwell on to scare you from even getting a quote. Remember your broker makes a lot less (75%) if you use a PEO.

Is the Technology Really Integrated?

Will a PEO integrate with your existing accounting and point of service systems?

This is right to the point. It’s not selling you want from your PEO, it’s not an “I’ll tell you all the great things I can do and show you all the things you gotta lookout for” situation – but don’t forget as you’re reading this that they really are great and they really do amazing things. The purpose of this is to make you realize that the shopping process itself and the selection process is fundamentally important to decide, whether you decide, to use a PEO in the first place, and which PEO to choose.

Technology Changed EVERYTHING:

In the past, most PEO‘s were not really fully integrated. The systems just really didn’t work well together even if they were the same platform, and most were simply a patchwork of systems.

Now many – but definitely not all – have fully integrated systems that: Are user-friendly, easy to implement, and seriously help with running a business.

Why Should Business Owners Opt for PEO Services?

This industry now has middlemen that actually tell you the truth! They save you money, cut out the expensive direct sales-y sales rep, and pass on the wholesale rates they get from the PEO’s. In addition to that, they know who is good and bad and why – and they’ll save you tons of time making sure you don’t pick the wrong one!

What are the most Important Differentiators

- Who has the service model you want and who has the technology that really makes it user friendly for you and your employees?

- Who really does have good long-term medical and workers comp renewals?

What they’re not is an insurance broker that doesn’t know anything about HR or payroll.

They are not a payroll company that doesn’t know about HR or Benefits. Think of a PEO as an HR company that also does payroll, HR technology, and all the expertise of HR. PEOs are the iPhone of human capital with people behind them that enables you to run your company better and safer and much less expensively.

Are PEO‘s Companies that can Provide PEO Employee Leasing Services?

Well, that’s how it all started – they were originally staffing companies, staffing agencies, employment agencies, private employment agencies, temp agency, or employee leasing companies that primarily operated in employee leasing services. What is a staffing agency? A staffing agency is an organization that has a list of employees that can be hired out for temporary or long term work. They provide staffing for any company looking to fill a position. Sometimes they were even used to play recruiting companies to assist businesses in getting Worker’s Comp. When the state wouldn’t provide it or for highly paid doctors who wanted to get defined benefit plans and pensions for themselves but not give it to their employees.

The concept originated in the 1960s by three businessmen – Eugene Boffa, Louis Calmare, and Joseph Martinez, but was further popularized by Marvin R. Selter.

Today all of that has changed, and the industry is the valve to take the big step from small business to professional, to have the ability to focus your time on building your company into what you have always dreamed it could be.

Are temp agencies worth it and other staffing companies worth it? PEO employee leasing allows you to put an end to all the headaches of employee benefits and insurance management, allowing you to scale your company, take care of your workers and get better prices for all of your employee care plans across the board.

What is a PEO Consultant or PEO Consulting Company or PEO Consulting Firm?

Well in most industries consulting companies generally charge fees and provide canned answers. They have a list of questions and a list of answers that go to those questions, and you usually get some type of generic or automated response when you want to go deeper into what’s included with these fees.

PEO consulting services may seem complex or confusing, but what we really are is a bridge. There are companies that want to help the businesses they work with get the best programs for their employees, and businesses who want their employees to be taken care of and their business to be secure – and we connect the two and eliminate the stress and headaches of trying to figure out who to trust.

We’ve been doing it for years, DECADES even. We know the ins and outs of PEOs and collaborating with them to ensure the best of both worlds, keeping you from being taken advantage of (especially since you usually don’t realize you are until it’s too late). With us, you’re dealing with real, experienced PEO consultants that know what they’re doing & know how to do it.

Our team has always been a brokerage company. We don’t charge fees and only earn our money if we find options that are great for you. We don’t just sign clients to get paid off of fees, we genuinely care about getting the best for you and the people you’re responsible for taking care of. Our PEO Consulting services are designed around simple aligned objectives with you and your company.

It’s not billable hours and time – it’s results we deliver, or we don’t get paid. We aren’t into PEO consulting for the money, we’re into it for the better options we’re able to get for businesses to take care of their employees, the better conditions their workers are able to secure for them. Better conditions mean better moods, better moods mean better work, better work means more profit & sales – so basically just making one small change and selecting the right PEO can be a snowball effect that can advance your company.

We are Objective. We are in this for one thing, to help businesses take better care of their people. We are PEO Consulting done right – not caring about the vendor, but only caring about our clients. We are into negotiating and getting the best deal, not just spreadsheeting and putting you on a client list – but getting together with you and talking about the real practical truth in each of the cells of a spreadsheet and the best way to get the plans that do the most for you.

All that being said beware of those companies that are PEO consulting services and charge for overly academic analysis, sometimes all of those big words and terms are meant to confuse and distract you from the fact that they really don’t know what they’re talking about in-depth.

If someone can’t explain their services to you in a way that a 5th grader can understand, there’s a good chance they don’t understand it enough themselves and are just repeating what they heard from somewhere else. Which would you rather have – someone trying to fool you with complex charts and big phrases, or the straightforward real experience and practical answers of multiple clients with multiple PEO’s with YEARS in the business?

The choice is obvious, isn’t it?

Differences Between PEOs

There are 700 and growing, and our guess is you should do business with about 650 of them. Of the 50 left you have some that specialize, while others are local, and you even have some that are national – some have great service, some have great technology, some a history of great renewals, others are about to be purchased, there are some that hide so many fees you will never know about, some are CPEOs (see the FAQ on this), some are putting in new i.t. systems, some were good last year and now omg they are so terrible it’s baffling and– wow that was a mouthful.

So, in short, they all will tell you they do everything a PEO should do, but most don’t and most just don’t do them well. Basically it’s like most businesses, but because this one encompasses so many aspects (things like medical, PTO, 401k, payroll, OSHA, etc) the worst thing you can do is pick the wrong one and end up having to switch the next year. Finally, once again we must caution you – the direct reps from the PEO’s are paid a lot and to do one thing – sell you the PEO they are working for that year. A Broker informant spills ALL!

So, get objective advice from a Broker.

Will I Loose Control of My Business?

Of course not! A PEO eliminates the annoying and expensive parts of running a business so that you can focus on growing your business.

It all started originally as staffing companies or employee leasing companies that primarily operated in employee leasing services. Sometimes the PEOs were even used to play recruiting companies to assist businesses in getting Worker’s Comp. When the state wouldn’t provide it or for highly paid doctors who wanted to get defined benefit plans and pensions for themselves but not give it to their employees.

Today a PEO has the ability to focus your time on building your company into what you have always dreamed it could be.

Do PEOs have Expensive Employee Contributions?

Do PEOs charge more for the employee contributions?

All the medical plans are presented the same – the real answer is they’re all different than what you have and it’s annoyingly complicated to compare them especially when you’re shopping more than one PEO. A Broker will help you compare different PEO options side by side in order to select the best fit for you and your employees.

Do PEOs Protect Us From Fines, Penalties, and E.R.I.S.A. Violations?

You are going to get sued as an employer – that is the world, unfortunately. Running a business with employees is really hard and the state, federal and even local laws continue to carry more enforcement and bigger penalties – and that’s before we get into form violations in PTO, overtime, sex discrimination, pay discrimination, 1099 vs. w-2 suits, Job offering, ACA reporting, etc.

PEOs actually protect you from most of this – their HR and legal staff are there to help you avoid these suits (even class-action suits). They protect you three ways actually; The Call – how do I fire this person without getting sued, The Documents – policies and documents in place in advance to pre-empt suits and protect you, and actual HR lawsuit insurance protection called EPLI coverage. Lastly, they don’t just do it because they say they will like some vendor – they are actually liable also and will be sued along with you, so they have skin in the game to protect both you and themselves.

Stay up to date by subscribing to our Free Stuff page where we constantly update new documents and information you need to know.

Read about the new E.R.I.S.A. Court Ruling that could make you personally liable.

Read about the New Executive Order Addressing Healthcare Issues.

2019 Compliance Digest.

DOL Penalties increased for 2019

How Can a PEO Broker Save Me Money?

Why is a PEO Cheaper Than Going Directly to an Insurance Company?

Why is a PEO cheaper they going directly to an insurance company for the same health insurance with the same insurance company?

- Size Does Matter: PEO’s are the largest medical buying groups for health insurance in America. They have over $11 Billion Dollars in buying power and under federal act (unavailable to your insurance broker) a PEO can aggregate the groups together for better negotiations and other cost efficiencies. Your insurance agent cannot even if they are giant and even if you love them.

- Swim in a clean pool! When your broker shops your benefits with the few carriers left in your area, the ACA requires them to take all companies – good risks and bad risks at mostly the same rates (age adjusted). PEO’s don’t have to take the bad risks! The skim the good risks. So, if you can get in that claims pool you are golden. PEOs therefore have much better claims experience – and therefore the rates are significantly less then then when your insurance broker gets you rates your own. Another important note – because of this not only are the rates lower when you join the PEO BUT their renewals tend to be half that of the private market – and that compounding is really important to your bottom line and employee satisfaction and retention.

- Lastly, because PEO’s provide a fully integrated HRIS – payroll, benefits, administration, enrollment, compliance (not just benefits compliance but full HR compliance – you know protection from the HR stuff you might/will get sued about – hiring, workplace stuff, fmla, overtime, terminations) and education service – it’s much more efficient for the insurance companies and for you – generally 20 to 30% less than your current costs!

Really, what do you have to lose by getting a quote?

(PS your insurance broker doesn’t want sell you a PEO – they get 90% less commission plus it is not really their business)

Are there other nickel and dime fees we need to know?

The answer can be yes – another reason you really need a professional to let you know all this and which PEO’s have what fees you may not know to even look at. Often when people receive the quote they ask if that includes health insurance, Worker’s Comp and unemployment and the answer to that is no.

But what about Administrative fees?

PEOs really have an extraordinary range – they can be anywhere from $49 per month per employee to over $150 a month per employee. Yes, that sounds high but remember you probably save way more than that on the Medical, Workers Comp and Unemployment. Some PEOs also charge a percentage of a payroll basis, and this is often the best pricing model for those companies with lower-paid employees. Those costs might range from 2 to 3.5% of payroll. (some also charge by check)

So do PEOs actually save you money?

The answer is usually yes, however not always. It depends on what you’re spending on health insurance, participation in your plans, etc. They generally can save a lot of money, buy it varies depending on your situation. But, the truth is you never know, and it’s worth the effort to get quotes because sometimes it’s dramatically cheaper. Choose an experienced PEO broker to help figure this out – they are objective, actually save you money, and save you from having to talk to 5 different PEO salespeople and finding the right PEO’s to compare.

Is 6% Renewal Acceptable?

My group health insurance renewal is only 6%, why would I get another quote? Isn’t that a great renewal?

It’s amazing how U.S. business owners have been brainwashed to believe that 6% is acceptable, or even great. 6% is three times more than inflation and it’s starting from a price that’s probably 20% too high in the first place.

You may think that because every year your broker’s shops the few insurance markets left and no other insurance broker has done much better and you like your broker – so why bother – that is the way it is – high prices and you are trapped?

PEO Brokers have $11 billion in premium behind them, your competitors use them, but your insurance broker does not (and cannot).

Employee Benefits is one of your largest expense line items, one of your most important retention tools, one of your most important hiring arrows and you need to make sure it’s always as sharp as can be.

By the way, if you get another quote from a PEO Broker your broker will not know that you’re shopping or looking for alternatives behind their backs – this is important to a lot of people.

4 Reasons to Use a PEO Broker

UP TO 20% LOWER ADMIN, MEDICAL, AND WC FEES. HOW?

1 – We cut out the expensive direct salesforce that generally makes up to 20% of the fees that they charge you.

2 – Our sales volume and contracts give your company complete access to our wholesale channel rates.

3 – Because the PEO’s know we shop the coverages and because of our ability to negotiate, we make sure you get all the modules and price breaks available at no extra cost to you.

And 4 – Our personal relationships with the salespeople and the PEO executives enables us to get you the best rates.

P.S. This is really important when you really need help in finding a solution to a service problem in the future.

Here is an example of a company that we had to go directly to a major PEO, and then we went to that PEO independently through the wholesale channel – look at the price differences!

So, Does a PEO Broker Save Me Money?

PEO Brokers have the clout to get you to lower admin rates, lower set up fees, lower medical costs, and lower worker’s comp costs. They leave no stone unturned and have decades of experience choosing the right services for you, getting the modules you wouldn’t normally get! They tell you everything you can get and make sure nothing is left out, while also getting them for less than the PEO direct salesperson (who you will never see again after the sale) would!

They’re a big franchise supermarket chain – they couldn’t care less about the average, daily customer as their way of thinking is “We’ll just get more,” but we treat you like family, like a valued member of the community.

Because that PEO salesperson is only representing a single company, they will only try to steer you toward their direction. They aren’t telling you what is inferior with their only product, and they’ll do whatever it takes to turn you into just another client on their list. It’s easy to overlook the problems they have if they hide all of them from you in the first place. You need to go to the people who care about getting the best for you and your employees. Macy’s doesn’t sell Gimbels.

The difference between a PEO Broker is they will treat you like a person, while a regular salesperson will just treat you like another client on a spreadsheet. Once you sign on the dotted line with that salesperson that’s usually the last you’ll see of them. They’ve got 299 more customers to sign-up and you’re immediately put on the backburner.

PEOs for Dummies

Why Should I Call a PEO Broker Instead of the PEO’s Directly?

You would think going directly to a provider is the least expensive way to shop – but it isn’t, and here’s why.

- Direct sales forces are very expensive – see below for more on how much they cost you. Buying through large channel partners is almost always guaranteed to be less expensive, and give you a better deal. Amazon, Wayfair, Hotel Tonight, Priceline, etc.

- A direct rep only sells that company, and once you call them and get in the PEOs salesman’s Retail pricing Sales system, you are often stuck at higher prices. Don’t get sucked into the rabbit hole before it’s too late!

- Direct sales reps have quotas – the more they charge you the more they make and the closer they are to their quotas. When they’re talking to you, they don’t care about you or your business, they just want to hurry up and close a deal so they can move on to the next unsuspected business owner.

- Direct sales reps don’t have the buying power of a large distributor – see below how much this can cost you in all the fees.

- Direct sales reps can only sell one company – so with that being said do you really think they’ll keep you up to date on that company’s issues, or just recommend one that is better?

- For example – when times get tough they conveniently “forget” to tell you about how they just lost a lot of clients and/or staff, how the modules really aren’t fully integrated, how they’re about to be sold, the ‘new’ software isn’t working well, a bad block of renewals is coming, e They’ll string you along for a client until the absolute last day, and then leave you hanging.

- Do you think they are going fairly spreadsheet all the competition (all fees, services, medical plans) and break it down in a way that lets you accurately see the best option out of all of the ones you have? No – you’ll have to do all of these comparisons on your own and learn how to do it right. The problem is, doing it right isn’t actually the easiest thing to do unless you know the behind the scenes real facts on this business game-changing decision)

- Do you think they will negotiate with all the other competitions as hard as a large distributor? Do you think they even have the power to? (hint: they don’t).

- You use brokers now – for medical, and workers comp – for a good reason. Would you hire someone who’s just painted a small shed in his backyard to paint your house, or would you rather hire a fully serviced professional painting crew? That’s the difference.

- Don’t call direct and get stuck paying retail. As soon as they answer the phone their one objective is to get you added to a spreadsheet as another client, paying way more than they should for a lot less of the services than they should be getting.

- Don’t call direct – People get stuck on average spending 63 hours talking to each direct rep, looking at their demos, and comparing everything. 63 Whole hours? You would definitely be better off spending all that time optimizing and expanding your business, wouldn’t you? That’s almost 3 days’ worth of time just trying to find the right PEOs and Services when you could meet with a broker and get it done in a fraction of the time!

Want to compare PEOs? Click here to view a sample of potential savings.

Top 5 Reasons People DON’T Get PEO Quotes?

- Their broker told them they are terrible.

- They don’t want to spend the time on getting another quote (p.s. it doesn’t take a lot of your time if you use the right PEO broker).

- They love their broker and think PEOs are like getting quote from another insurance broker (but it is far from that – it is accessing bulk buying that your broker doesn’t have access to and doesn’t want you to know about.

- You got a quote years ago and it wasn’t good – (but the industry has changed dramatically after the federal act came out to regulate this industry and technology has allow you do things you couldn’t before, and the private market health rates still keep going up.)

- A major reason to get these quotes is honestly it is your job and now the courts have just made you actually personally liable if you don’t make sure you get the best deals for your employees under ERISA.

Are There Differences in PEOs Other than Price?

There are 700 and growing, and our guess is you should do business with about 650 of them. Of the 50 left you have some that specialize, while others are local, and you even have some that are national – some have great service, some have great technology, some a history of great renewals, others are about to be purchased, there are some that hide so many fees you will never know about, some are CPEOs (see the FAQ on this), some are putting in new i.t. systems, some were good last year and now omg they are so terrible it’s baffling and– wow that was a mouthful. So, in short, they all will tell you they do everything a PEO should do, but most don’t and most just don’t do them well. Basically it’s like most businesses, but because this one encompasses so many aspects (things like medical, PTO, 401k, payroll, OSHA, etc) the worst thing you can do is pick the wrong one and end up having to switch the next year. Finally, once again we must caution you – the direct reps from the PEO’s are paid a lot and to do one thing – sell you the PEO they are working for that year.

What Businesses Can Use a PEO?

PEOs have plans for every vertical.

Including:

- Technology

- Manufacturing

- Medical

- Staffing

- Hospitality

- Venture Capital

- and so many more!

PEO Broker Underwriters have quality providers in every vertical and industry – in every state, and every size from 25 to 5,000 employees.

Will I Loose Control of My Business?

Of course not! A PEO can eliminate the annoying and expensive parts of running a business so that you can focus on growing your business.

It all started originally as staffing companies or employee leasing companies that primarily operated in employee leasing services. Sometimes the PEOs were even used to play recruiting companies to assist businesses in getting Worker’s Comp. When the state wouldn’t provide it or for highly paid doctors who wanted to get defined benefit plans and pensions for themselves but not give it to their employees.

Today a PEO has the ability to focus your time on building your company into what you have always dreamed it could be.

{kind=link}

{kind=link}